VWAP Indicator Explained: The Intraday Fair-Value Line

VWAP indicator explained in plain language: what it measures, how to read it, the signals it gives, and how to use it inside a no-code automated trading bot.

What VWAP actually measures

VWAP (Volume-Weighted Average Price) is the average price an asset has traded at during the session, weighted by volume. Unlike a simple moving average, it gives more weight to prices where lots of contracts or shares changed hands.

The result is a single line that represents the session's volume-weighted "fair value." Price above VWAP means buyers, on average, are paying up; price below means the average participant got in cheaper.

VWAP is an intraday tool. It resets at the start of each session, so it's most meaningful on short timeframes (1m–15m) and loses its standard meaning on daily or weekly charts.

How to read the VWAP line

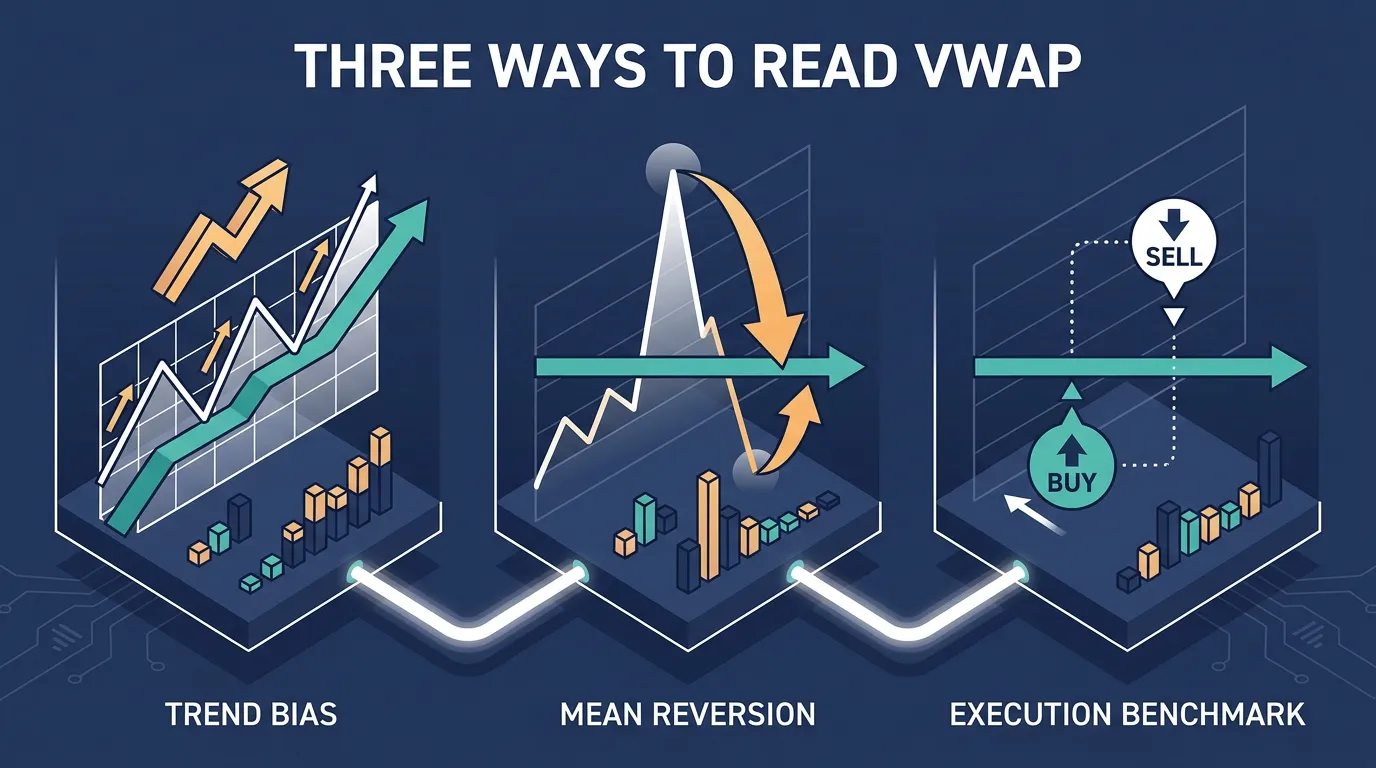

VWAP is used three main ways:

- Trend bias. Price holding above a rising VWAP suggests bullish control for the session; price pinned under a falling VWAP suggests sellers dominate. Many intraday traders simply avoid longs below VWAP and shorts above it.

- Mean reversion. When price stretches far from VWAP, it often snaps back toward it. Traders fade extreme moves expecting a return to the average.

- Execution benchmark. Institutions judge fills against VWAP — buying below it or selling above it is considered a good entry. Retail traders borrow the same logic for cleaner entries.

A common refinement adds VWAP bands (standard-deviation envelopes around the line) to flag when price is statistically stretched.

The cleanest VWAP signal isn't a cross — it's a retest: price pulls back to VWAP, holds, and resumes in the prevailing direction.

Strengths and limits

VWAP's edge is that it bakes in volume, so it reflects where conviction actually sits — not just where price closed. That makes it a favourite for liquid markets and intraday strategies.

VWAP is a lagging line built from the session so far. Early in the session it's noisy and sensitive to a few large trades — give it time to stabilise before trusting it.

Because it's session-bound, VWAP works best on instruments with clear, consistent volume — major crypto pairs, liquid US stocks, and active forex hours. In illiquid names the line can be dragged around by single large prints.

Using VWAP in a no-code bot

On algomax you don't code any of this. You describe the rule in plain language and the AI assistant turns it into a ready-to-run bot. For example, you might say you want to go long only when price is above VWAP and pulls back to touch it, with a stop just beneath the line.

A practical workflow:

- Set the bias — only trade in the direction relative to VWAP (longs above, shorts below).

- Define the trigger — a retest of VWAP, or a stretch to an outer band for mean reversion.

- Add risk controls — a stop referenced to VWAP and a sensible position size.

- Backtest first. Because VWAP resets each session, always before going live.

Once you're satisfied, the runs continuously through your own connected broker keys, applying the same VWAP logic without you watching every candle. Pair it with a momentum filter like RSI to avoid fading strong trends.

Key takeaways

- VWAP is the volume-weighted average price for the session — an intraday fair-value benchmark.

- Read it for trend bias, mean reversion, and execution quality; bands flag stretched price.

- It's session-bound and lagging — best on liquid, intraday timeframes, weak on daily charts.

- On a no-code platform you describe a VWAP rule in plain language, backtest it, then run it as an automated bot.

Frequently asked questions

What is the difference between VWAP and a moving average?

A moving average treats every price equally, while VWAP weights each price by the volume traded there. That makes VWAP a better gauge of where real conviction sits, but it also resets each session, whereas a moving average runs continuously across days.

Is VWAP only useful for day trading?

Largely, yes. Standard VWAP resets at the start of each session, so it's designed for intraday timeframes. On daily or weekly charts it loses its usual meaning, though some traders use anchored variants tied to a specific event instead.

Can VWAP be used for both trend and mean-reversion strategies?

Yes. Traders use price relative to VWAP as a trend bias filter, and they also fade large stretches away from VWAP expecting a snap back toward it. Adding standard-deviation bands helps identify when price is statistically stretched.

Do I need to code to use VWAP in an automated bot?

No. On a no-code platform like algomax you describe your VWAP rule in plain language and the AI assistant turns it into a ready-to-run bot. You can backtest it on historical candles and then run it live through your own connected broker keys.

Does VWAP work in low-volume markets?

It works best in liquid markets with consistent volume. In thin, low-volume instruments a few large trades can drag the VWAP line around, making its signals less reliable, so it's safest on active pairs and busy trading hours.