Backtest Before You Go Live With a No-Code Bot

Learn how to backtest a no-code trading bot on historical candles before risking real money, what results actually mean, and the pitfalls to avoid.

Why backtest before going live

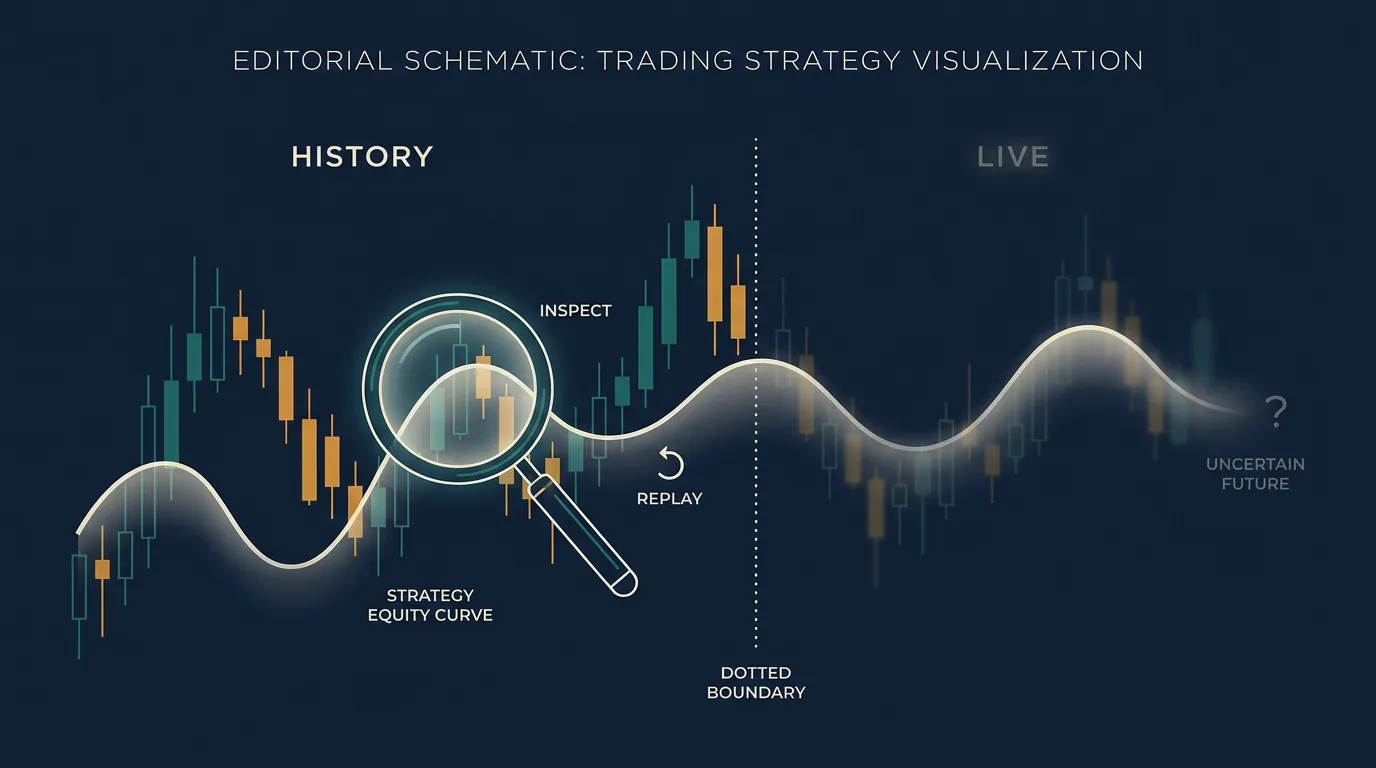

A backtest replays your strategy against historical candles to show how it would have behaved. With a no-code platform, you describe the idea in plain language, the AI turns it into a runnable bot, and you test that bot on past data — all before a single real order is placed.

The point isn't to find a "winning" strategy. It's to catch obvious flaws, sanity-check your logic, and understand a strategy's behaviour — how often it trades, how deep its losing streaks run, how it reacts to choppy markets — while mistakes are still free.

A backtest tells you what a strategy did on old data. It never promises what it will do next.

What a backtest actually measures

Run a test and you'll get a set of metrics. The headline number — total return — is the least useful one in isolation. Look instead at the shape of the results:

- Max drawdown — the worst peak-to-trough drop. This is your gut-check for whether you could stomach the strategy live.

- Number of trades — too few and the result is luck, not edge. A handful of trades proves nothing.

- Win rate vs. average win/loss — a 40% win rate can be excellent if winners dwarf losers. Don't judge win rate alone.

- Consistency across periods — does it work only in one bull run, or across different regimes?

Compare your strategy against simply holding the asset over the same window. If it can't beat buy-and-hold after costs, the added complexity may not be worth it.

Pitfalls that make backtests lie

Most backtests look better than reality because of avoidable errors. Watch for these:

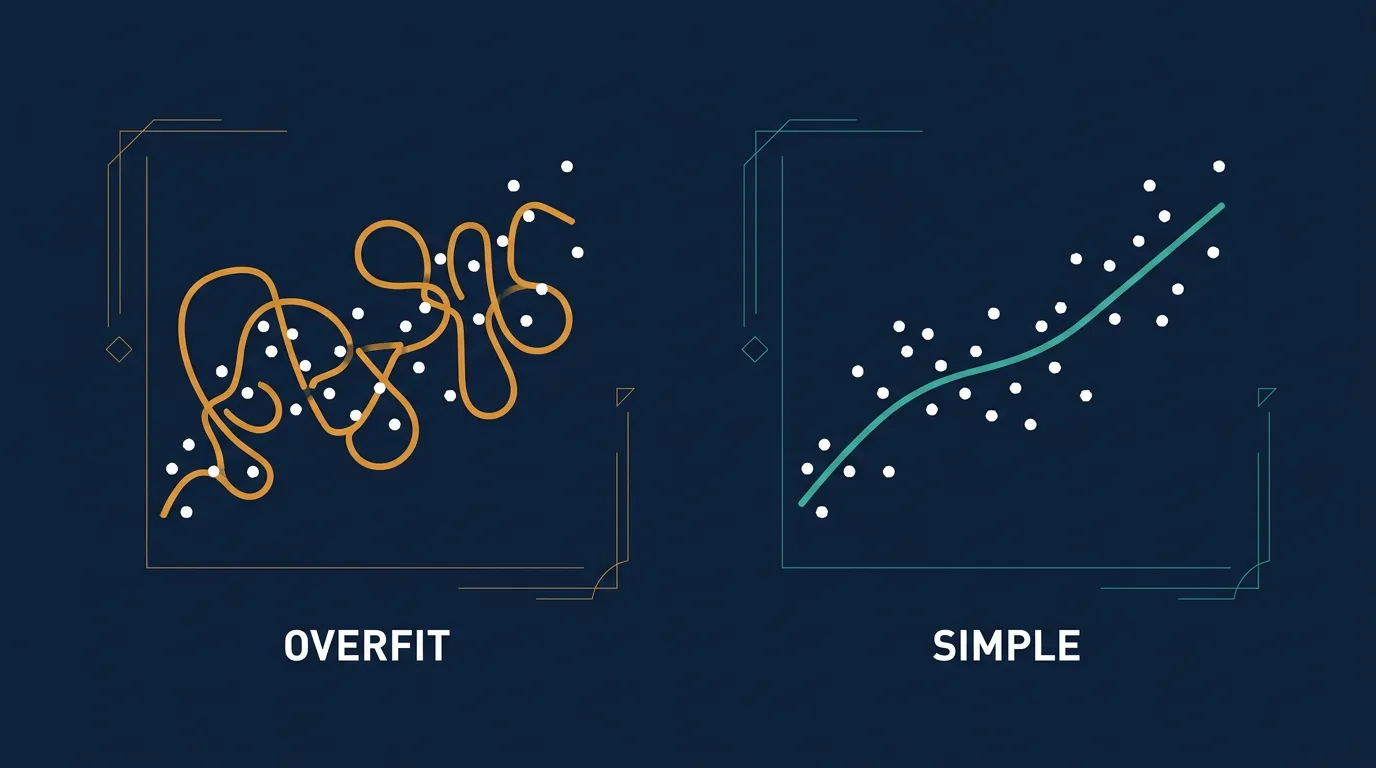

The most seductive trap is overfitting: you keep adjusting thresholds until the equity curve looks beautiful. A strategy with five tightly-tuned conditions usually performs worse live than a simpler one with two robust rules. When in doubt, prefer fewer moving parts.

A flawless backtest is a red flag, not a green light. Real markets include gaps, slippage, and conditions your test never saw. Treat strong results with healthy skepticism.

To stress-test honestly, run the strategy across multiple market regimes — a trending stretch, a sideways chop, and a sharp drawdown — rather than one clean uptrend. If it survives all three, you've learned something real. Because keeps the describe-test-deploy steps in one flow, iterating on the plain-language description and re-testing takes minutes, not a rewrite.

From a clean test to a cautious live run

A good backtest earns a strategy the right to trade small, not the right to trade big. Bridge the gap deliberately:

- Re-test on a recent, untouched period you didn't use while tuning.

- Add realistic costs so the numbers reflect your broker, not a fantasy.

- Deploy with minimal size through your own connected broker keys and watch live behaviour match — or diverge from — the test.

- Keep notifications on so you see fills and exits as they happen.

Live trading introduces frictions a backtest can't fully model, which is exactly why you start small. You can explore plans and limits on the , or read more about the platform's approach on the .

Key takeaways

- Backtest to understand behaviour and risk, not to chase a perfect return number.

- Focus on drawdown, trade count, and consistency over headline profit.

- Overfitting and omitted costs are the top reasons tests mislead.

- A passed backtest justifies a small, monitored live run — never a guarantee.

Frequently asked questions

Does a good backtest mean my bot will be profitable live?

No. A backtest only shows how a strategy behaved on past data. Real markets bring slippage, gaps, and conditions the test never saw, so strong historical results are no guarantee of future performance.

How many trades should a backtest include to be meaningful?

There's no magic number, but a handful of trades is statistically meaningless. You want enough trades across different market conditions that the result reflects a repeatable pattern rather than luck.

What is overfitting and how do I avoid it?

Overfitting is tuning rules until they fit past data perfectly, which usually breaks on new data. Avoid it by keeping strategies simple, testing on periods you didn't tune on, and being suspicious of flawless results.

Do I need to code to backtest on algomax?

No. You describe your strategy in plain, conversational language and the AI turns it into a runnable bot you can backtest on historical candles, then deploy live through your own broker keys — without writing or seeing any code.

Should I include trading costs in a backtest?

Yes. Fees, spread, and slippage can turn an apparently profitable strategy into a losing one. Always test with realistic costs before considering a live run.